080: Will Australia’s Property Market and Economy Go Down Under? An Episode Featuring Steve Keen

This weeks episode of the Economic Rockstar podcast features the Australian economy. There is talk amongst economists, analysts and commentators, be it speculative or not, that the Australian economy or it’s housing market will implode within the next 12 to 18 months. I am joined with Professor Steve Keen who explains why the property market in Australia will crash, taking its economy down with it.

Given the nature of this podcast, I cannot ignore the discussion that is taking place on what’s going on with the Australian economy. To be honest, a listener to this podcast who is living in Australia contacted me on what’s going on there, and he and his friends are taking precautions in the event of a collapse in house prices. I also have Irish friends who emigrated to Australia once the financial crisis hit. These young men travelled from Ireland to Australia and know, with first-hand experience, how an economy and housing market performs prior to a crash. They, like others, are tuned into events that lead to a bursting of a bubble. Doubters and cynics may claim that this is an unscientific approach to analysing the market, but shouldn’t we also consider non-numeric data in the form of intuition and gut-instinct?

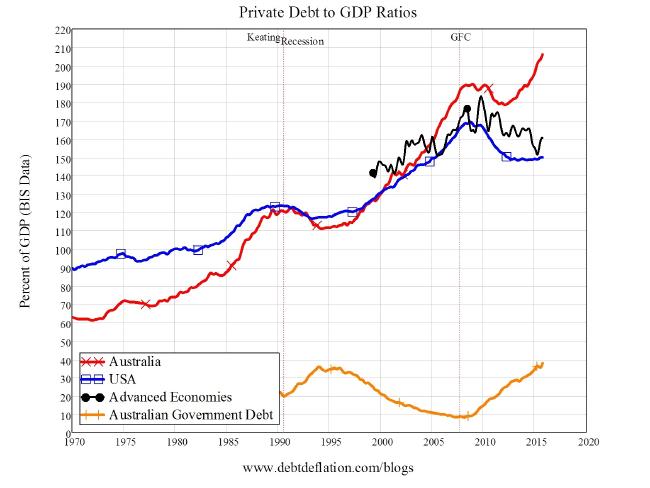

Economic data is also available today that supports the claim that the Australian housing market is on the brink of collapse. Australia’s private debt to GDP is currently at 210%, the highest in its history. Such high ratios were experienced by other developed economies prior to the Great Financial Crisis which pushed them into recession following a property market crash. Is Australia different? Australia is most definitely not immune to such crashes.

Did you know that house prices plunged 30 percent or more in NSW and Victoria in the 1890s and 1930s — the biggest such reversals in Australia’s history — the result was bank collapses and mass unemployment. Could this be repeated?

So a question I’d like to pose would be ‘What’s worse? Carrying out a pre-mortem or a post-mortem. Both can have very damaging repercussions for an individual if decision-making was wrong. A pre-mortem forces someone to take a contrarian view of the economy. They can then write up a checklist of possible events that could materialize and the actions that need to be taken today to assure a minimum negative impact.

Can a person’s pre-mortem be evidence of over-confidence or can it be a deep-rooted intuitive reading of all the vital signs that are indicating something sinister that had once played out before? After-all, many economies have experienced busts and housing market crashes. No country is immune to these events. What precipitates a housing crisis has been explained on numerous occasions in the economic literature, albeit for different time periods, economic cycles and, dare I say, personal viewpoints and data collection methods.

So, should we ignore the intuition and gut instinct of those in tune with the development of an economy and its actors? Is Australia different to other economies? After all, Australia hasn’t experienced a recession since 1991 – 25 years ago!

Should we ignore or heed the warnings of the naysayers? Can intuition be considered a valid barometer to understanding how events are likely to unfold in an economy?

Nobel laureate Danial Kahneman who, in an interview with McKinsey and Company, considered the intuition of professionals in the decision-making process. Kahneman stated that:

There are some conditions where you have to trust your intuition. When you are under time pressure for a decision, you need to follow intuition. My general view, though, would be that you should not take your intuitions at face value. Overconfidence is a powerful source of illusions, primarily determined by the quality and coherence of the story that you can construct, not by its validity. If people can construct a simple and coherent story, they will feel confident regardless of how well grounded it is in reality.

Despite this statement being considered under a different context, it could easily be applied to the economy since professionals are a subset of the population and their decisions can impact the local and wider economy.

Let’s break this statement down.

Kahneman states that “When you are under time pressure for a decision, you need to follow intuition.” In an economy or a housing market that is performing so well like Australia today, time doesn’t play a central role for the majority of those involved in the decision-making process. Of course, well-timed investments can be the difference between a gain and a loss.

Typically, in good times, people can become blind-sided and focus on the positive news. The economy will continue on as it has always done. The housing market will continue performing strongly and it will always be a good time to buy property. When you’re in the thick of it, the good times keep rolling. You want to participate in any market whose assets are experiencing capital appreciation. The majority of people make decisions based on past performance. The housing market in Australia has grown to unprecedented yet worrying levels.

Any negative news or commentary is largely dismissed and the bearers of the bad news are typically criticised and vilified. Humans have the ability to forget their past failings and fallibilities and repeatedly make the same mistakes over and over again. Economic history shows us the misconceptions and judgemental errors made by humans from Tulip Mania to the South Sea Bubble and the dot-com crash. If the housing market was to implode in Australia, time would become the main focus as people will rush to the exits. Housing is not as liquid as stocks or cash and a housing crash will be the result.

Participants in the Australian housing market are accumulating dangerous levels of private debt, never seen before in its history. Private household debt now stands at 210% of GDP. This is an unhealthy level for any economy to be in and one that was highlighted by Professor Steve Keen in his blog debtdeflation.com and his book Debunking Economics. Professor Keen warned of the risks to many economies and their housing market prior to the Great Financial Crisis.

Australia’s Private Debt to GDP Ratio as Calculated by Professor Steve Keen

He also warned about Australia’s economy at the time but Australia avoided a recession. Policy initiatives at the time, as well as the availability of credit, rising commodity prices (of which Australia benefits from), a demand for housing stock from mainland China and an appetite for risk to avail of the speculative gains being made in an accelerating property market has resulted in Australia being different to other economies.

Australia is the darling economy and a perceived role model on how to maintain economic growth. These positives led to immigration rising as a demand for employment increased. And as we know, when jobs are created, income levels rise feeding the demand for goods and services. Eventually, confidence rises and speculative purchases are made. When the desired expectations to these speculative purchases come to fruition, then people become overconfident.

As Kahneman stated earlier, “Overconfidence is a powerful source of illusions, primarily determined by the quality and coherence of the story that you can construct, not by its validity. If people can construct a simple and coherent story, they will feel confident regardless of how well grounded it is in reality.”

RBA economist Peter Tulip last year suggested Australian housing could be as much as 30 percent undervalued. This type of commentary is not helpful in a market that is overheating and when participants or would-be buyers are excited about capital appreciation despite being negatively geared. This is definitely a new take on Tulip Mania!

The same economist, Peter Tulip, in a 2007 working paper for the OECD, wrote about how safe Iceland’s economy was and that it’s banking system was secure and stable, and that it’s housing market should be liberalised and opened up to competition.

Today, there are reports of being able to borrow 10 times your pre-tax income to purchase a property. This is not a healthy situation for anyone to be in, including banks.

What could be the catalyst to a housing market crash in Australia?

Australia has an active sub-prime mortgage market. Interest rates are low at 2% (yet they could go lower as we have seen elsewhere). Perhaps the Royal Bank of Australia isa keeping a 2% cushion in the event of implementing a loose monetary policy in the event of a crash. Unfortunately, this type of stimulus will not work as households will be required to pay down its debt and the economy could enter into a Japanese-style era of stagflation.

Australia is dependent heavily on its commodities, hence the dollar being know as a commodity currency. There is a continuing drop in resource prices and commodity-dependent companies such as Rio and BHP are in trouble.

Banking shares have dropped and could be seen as ominous of what’s to come. Are there people in the know? Are they liquidating their holdings? Check out what happened to many of the leading US and European banking shares prior to October 2008 – the official start of the Great Financial Crisis. They were already on a downward trajectory.

Is China slowing down? The Chinese have also accumulated high levels of private debt and their private debt to GDP ratio is similarly high to Australia’s. If Chinese investment in the Australian property market stops, then the market could implode.

There is an overwhelming supply of apartments in Brisbane, Melbourne and Sydney. Many of these apartments lie vacant and buyers are expecting their negatively geared position to be offset by further capital appreciation. Also, immigrants have proven to be very mobile. When signs of a weakening economy materialise, they will emigrate leaving a slump in housing or rental demand. Owners will fail to meet repayments as the main source of their rental income will disappear.

Put simply, in the words of Professor Steve Keen, Australia’s housing market is a Ponzi scheme and those that got in first will be the winners while all of those who got in over the last few years will suffer.

Links:

- www.debtdeflation.com/blog by Steve Keen

- Get Ready for an Australian Recession by 2017 – Steve Keen

- Strategic decisions: When can you trust your gut? McKinsey and Company interview with Daniel Kahneman and Gary Klein.

- Tulip, P. (2007). Financial Markets in Iceland. OECD. Working Paper No. 549.

- Fox, R. and Tulip, P. (2014). Is Housing Overvalued? Reserve Bank of Australia.

Books:

- Debunking Economics by Steve Keen

Podcast: Play in new window | Download